Talk to the experts

Learn more about Extend and find out if it's the right solution for your business.

June 23, 2026 8:00 PM

Most finance leaders have had the same experience: a company card program that was supposed to simplify things, but became its own administrative burden. Employees carry cards with shared limits, receipts go missing, and month-end reconciliation means hours of spreadsheet work trying to match charges to departments or projects.

The problem isn't that teams spend too much. The problem is that most card programs weren't built with finance teams in mind. Recent payment industry research found that the majority of cardholders, including business cardholders, feel indifferent or actively dissatisfied with their card experience. For personal spending, that might be a minor frustration, but for finance teams managing hundreds of transactions a month, it's a real operational problem.

Here's what's actually driving that dissatisfaction, and what a better card experience looks like for the teams managing business spend.

When CFOs and controllers describe their ideal card experience, the requests are remarkably consistent. They want to know who spent what before the month ends — not when the statement arrives. They want to issue spending authority quickly without handing out a shared corporate card. They want receipts collected automatically, not chased the week before close. And they want reconciliation to happen at transaction time, not billing time.

These aren't exotic requirements. They're the basics of financial control. But traditional card programs tend to deliver individual spending records without the workflow layer finance teams need. As we explored in one of our latest blog posts, real-time expense treal-time expense tracking: benefits beyond just visibility, the gap between when a transaction happens and when finance knows about it is where most expense management problems originate.

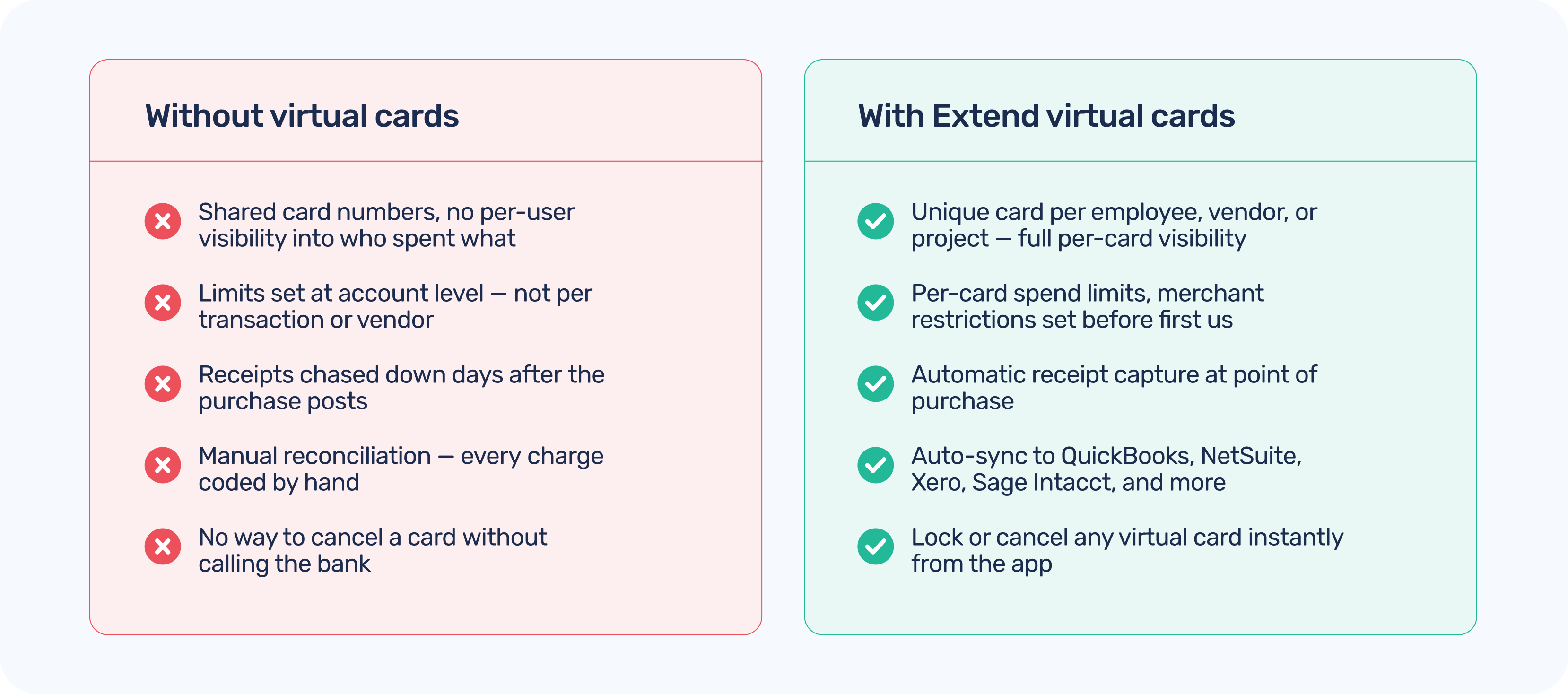

Traditional card programs have a few structural limitations that create ongoing friction for finance teams:

The result is a card program that generates data without generating control, which is precisely the opposite of what finance teams are trying to build.

Virtual cards are often described as "digital versions of physical cards", but that framing undersells what they do for finance teams. The meaningful difference isn't the format. It's the control layer.

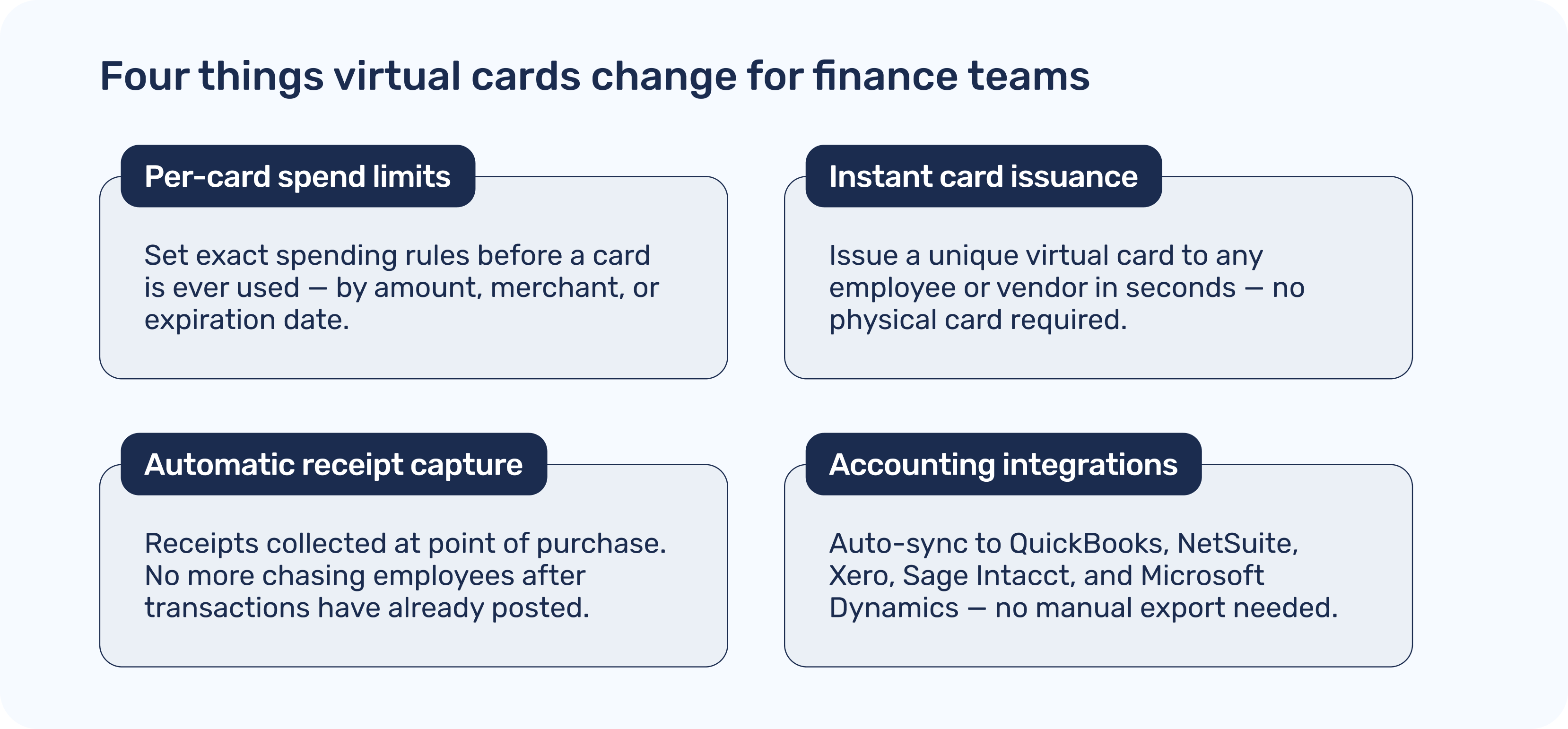

With virtual cards through Extend, finance teams can issue a unique card to any employee or vendor in seconds, with per-card spend limits and expiration dates set before the card is ever used. When a charge posts, the receipt is already attached. When it's time to reconcile, the transaction flows automatically to your accounting system — whether that's QuickBooks, NetSuite, Xero, Sage Intacct, or Microsoft Dynamics.

This is what streamlining expense management actually looks like in practice: not just reporting on what happened, but controlling what can happen in the first place.

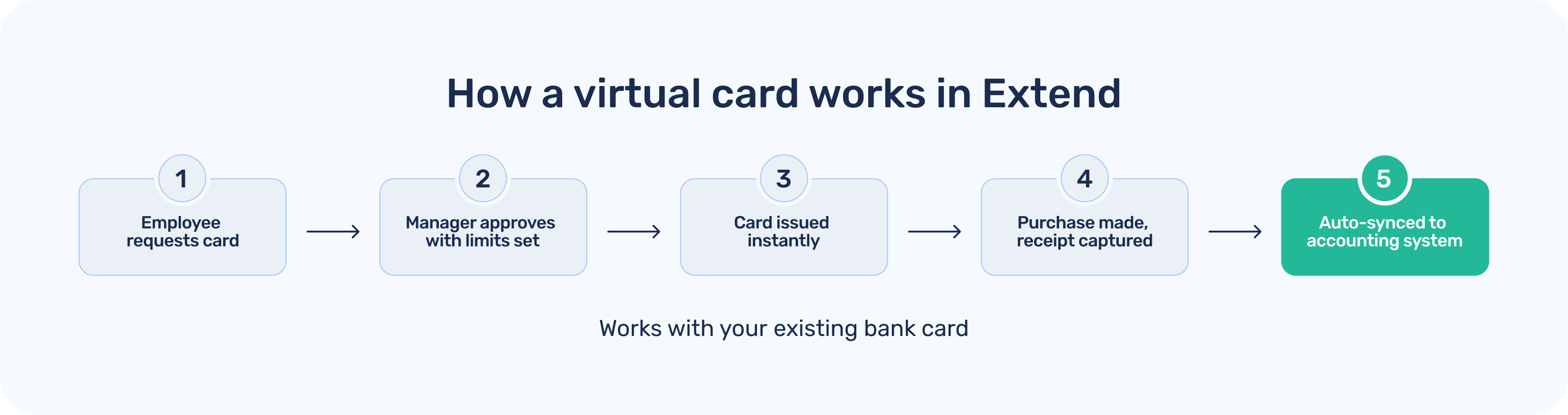

One of the most meaningful shifts virtual cards enable is connecting the full lifecycle of a business payment — from approval to reconciliation — without requiring finance to manually stitch together multiple systems.

With Extend, when an employee needs a card for a vendor or project, the request and approval happen in the app. The card is issued with the right limits already embedded. When the charge posts, the receipt is already attached. When it's time to close the books, transactions flow automatically to your accounting system.

The key shift is that work traditionally done at month-end — coding, categorizing, matching — gets distributed to the point of purchase, where context is still fresh and receipts are right at hand.

Extend also works on top of the business credit cards your company already has. That means you keep your existing bank relationship, your rewards programs, and your preferred credit lines. You're adding a control layer — not rebuilding your payment infrastructure.

Better card controls are only useful if they're enforced consistently. One reason expense policy compliance is hard to maintain is that policies live in a document, while spending happens in the real world — on travel booking sites, vendor portals, and online stores.

Virtual cards bridge that gap. When you issue a card with a specific limit, a specific vendor restriction, or a specific expiration date, the policy is embedded in the card itself. There's no room for an employee to accidentally overspend because the card simply won't authorize charges that exceed the parameters you've set.

This doesn't require employees to do anything differently — they use the card like any other credit card. The control happens at the infrastructure level, not through employee self-discipline. For teams building or updating their expense policies, expense policy best practices and templates for modern businesses walks through how to structure controls that work alongside virtual card programs like Extend.

For teams managing spend across multiple departments or locations, Extend also supports budget-level controls — grouping spend across multiple virtual cards under a single budget so you can see total burn against a project or cost center in real time.

The business card experience isn't just about the card itself — it's about the entire workflow surrounding how money moves through your organization. Most card programs deliver a payment mechanism. What finance teams need is a control layer.

Extend adds that control layer without requiring you to switch banks or rebuild your payment infrastructure. You keep your existing bank relationship, your credit lines, and your rewards programs. You add the per-card limits, real-time visibility, receipt capture, and accounting integrations your team actually needs to operate efficiently.

The result is a card program that works for finance — not one that creates extra work for it. Learn more about virtual employee cards with Extend and how spend controls give finance teams the oversight they need without slowing down the employees doing the spending.

Dawn Lewis

Controller at Couranto

Bridget Cobb

Staff Accountant at Healthstream

Brittany Nolan

Sr. Product Marketing Manager at Extend (moderator)

Most finance leaders have had the same experience: a company card program that was supposed to simplify things, but became its own administrative burden. Employees carry cards with shared limits, receipts go missing, and month-end reconciliation means hours of spreadsheet work trying to match charges to departments or projects.

The problem isn't that teams spend too much. The problem is that most card programs weren't built with finance teams in mind. Recent payment industry research found that the majority of cardholders, including business cardholders, feel indifferent or actively dissatisfied with their card experience. For personal spending, that might be a minor frustration, but for finance teams managing hundreds of transactions a month, it's a real operational problem.

Here's what's actually driving that dissatisfaction, and what a better card experience looks like for the teams managing business spend.

When CFOs and controllers describe their ideal card experience, the requests are remarkably consistent. They want to know who spent what before the month ends — not when the statement arrives. They want to issue spending authority quickly without handing out a shared corporate card. They want receipts collected automatically, not chased the week before close. And they want reconciliation to happen at transaction time, not billing time.

These aren't exotic requirements. They're the basics of financial control. But traditional card programs tend to deliver individual spending records without the workflow layer finance teams need. As we explored in one of our latest blog posts, real-time expense treal-time expense tracking: benefits beyond just visibility, the gap between when a transaction happens and when finance knows about it is where most expense management problems originate.

Traditional card programs have a few structural limitations that create ongoing friction for finance teams:

The result is a card program that generates data without generating control, which is precisely the opposite of what finance teams are trying to build.

Virtual cards are often described as "digital versions of physical cards", but that framing undersells what they do for finance teams. The meaningful difference isn't the format. It's the control layer.

With virtual cards through Extend, finance teams can issue a unique card to any employee or vendor in seconds, with per-card spend limits and expiration dates set before the card is ever used. When a charge posts, the receipt is already attached. When it's time to reconcile, the transaction flows automatically to your accounting system — whether that's QuickBooks, NetSuite, Xero, Sage Intacct, or Microsoft Dynamics.

This is what streamlining expense management actually looks like in practice: not just reporting on what happened, but controlling what can happen in the first place.

One of the most meaningful shifts virtual cards enable is connecting the full lifecycle of a business payment — from approval to reconciliation — without requiring finance to manually stitch together multiple systems.

With Extend, when an employee needs a card for a vendor or project, the request and approval happen in the app. The card is issued with the right limits already embedded. When the charge posts, the receipt is already attached. When it's time to close the books, transactions flow automatically to your accounting system.

The key shift is that work traditionally done at month-end — coding, categorizing, matching — gets distributed to the point of purchase, where context is still fresh and receipts are right at hand.

Extend also works on top of the business credit cards your company already has. That means you keep your existing bank relationship, your rewards programs, and your preferred credit lines. You're adding a control layer — not rebuilding your payment infrastructure.

Better card controls are only useful if they're enforced consistently. One reason expense policy compliance is hard to maintain is that policies live in a document, while spending happens in the real world — on travel booking sites, vendor portals, and online stores.

Virtual cards bridge that gap. When you issue a card with a specific limit, a specific vendor restriction, or a specific expiration date, the policy is embedded in the card itself. There's no room for an employee to accidentally overspend because the card simply won't authorize charges that exceed the parameters you've set.

This doesn't require employees to do anything differently — they use the card like any other credit card. The control happens at the infrastructure level, not through employee self-discipline. For teams building or updating their expense policies, expense policy best practices and templates for modern businesses walks through how to structure controls that work alongside virtual card programs like Extend.

For teams managing spend across multiple departments or locations, Extend also supports budget-level controls — grouping spend across multiple virtual cards under a single budget so you can see total burn against a project or cost center in real time.

The business card experience isn't just about the card itself — it's about the entire workflow surrounding how money moves through your organization. Most card programs deliver a payment mechanism. What finance teams need is a control layer.

Extend adds that control layer without requiring you to switch banks or rebuild your payment infrastructure. You keep your existing bank relationship, your credit lines, and your rewards programs. You add the per-card limits, real-time visibility, receipt capture, and accounting integrations your team actually needs to operate efficiently.

The result is a card program that works for finance — not one that creates extra work for it. Learn more about virtual employee cards with Extend and how spend controls give finance teams the oversight they need without slowing down the employees doing the spending.

Most finance leaders have had the same experience: a company card program that was supposed to simplify things, but became its own administrative burden. Employees carry cards with shared limits, receipts go missing, and month-end reconciliation means hours of spreadsheet work trying to match charges to departments or projects.

The problem isn't that teams spend too much. The problem is that most card programs weren't built with finance teams in mind. Recent payment industry research found that the majority of cardholders, including business cardholders, feel indifferent or actively dissatisfied with their card experience. For personal spending, that might be a minor frustration, but for finance teams managing hundreds of transactions a month, it's a real operational problem.

Here's what's actually driving that dissatisfaction, and what a better card experience looks like for the teams managing business spend.

When CFOs and controllers describe their ideal card experience, the requests are remarkably consistent. They want to know who spent what before the month ends — not when the statement arrives. They want to issue spending authority quickly without handing out a shared corporate card. They want receipts collected automatically, not chased the week before close. And they want reconciliation to happen at transaction time, not billing time.

These aren't exotic requirements. They're the basics of financial control. But traditional card programs tend to deliver individual spending records without the workflow layer finance teams need. As we explored in one of our latest blog posts, real-time expense treal-time expense tracking: benefits beyond just visibility, the gap between when a transaction happens and when finance knows about it is where most expense management problems originate.

Traditional card programs have a few structural limitations that create ongoing friction for finance teams:

The result is a card program that generates data without generating control, which is precisely the opposite of what finance teams are trying to build.

Virtual cards are often described as "digital versions of physical cards", but that framing undersells what they do for finance teams. The meaningful difference isn't the format. It's the control layer.

With virtual cards through Extend, finance teams can issue a unique card to any employee or vendor in seconds, with per-card spend limits and expiration dates set before the card is ever used. When a charge posts, the receipt is already attached. When it's time to reconcile, the transaction flows automatically to your accounting system — whether that's QuickBooks, NetSuite, Xero, Sage Intacct, or Microsoft Dynamics.

This is what streamlining expense management actually looks like in practice: not just reporting on what happened, but controlling what can happen in the first place.

One of the most meaningful shifts virtual cards enable is connecting the full lifecycle of a business payment — from approval to reconciliation — without requiring finance to manually stitch together multiple systems.

With Extend, when an employee needs a card for a vendor or project, the request and approval happen in the app. The card is issued with the right limits already embedded. When the charge posts, the receipt is already attached. When it's time to close the books, transactions flow automatically to your accounting system.

The key shift is that work traditionally done at month-end — coding, categorizing, matching — gets distributed to the point of purchase, where context is still fresh and receipts are right at hand.

Extend also works on top of the business credit cards your company already has. That means you keep your existing bank relationship, your rewards programs, and your preferred credit lines. You're adding a control layer — not rebuilding your payment infrastructure.

Better card controls are only useful if they're enforced consistently. One reason expense policy compliance is hard to maintain is that policies live in a document, while spending happens in the real world — on travel booking sites, vendor portals, and online stores.

Virtual cards bridge that gap. When you issue a card with a specific limit, a specific vendor restriction, or a specific expiration date, the policy is embedded in the card itself. There's no room for an employee to accidentally overspend because the card simply won't authorize charges that exceed the parameters you've set.

This doesn't require employees to do anything differently — they use the card like any other credit card. The control happens at the infrastructure level, not through employee self-discipline. For teams building or updating their expense policies, expense policy best practices and templates for modern businesses walks through how to structure controls that work alongside virtual card programs like Extend.

For teams managing spend across multiple departments or locations, Extend also supports budget-level controls — grouping spend across multiple virtual cards under a single budget so you can see total burn against a project or cost center in real time.

The business card experience isn't just about the card itself — it's about the entire workflow surrounding how money moves through your organization. Most card programs deliver a payment mechanism. What finance teams need is a control layer.

Extend adds that control layer without requiring you to switch banks or rebuild your payment infrastructure. You keep your existing bank relationship, your credit lines, and your rewards programs. You add the per-card limits, real-time visibility, receipt capture, and accounting integrations your team actually needs to operate efficiently.

The result is a card program that works for finance — not one that creates extra work for it. Learn more about virtual employee cards with Extend and how spend controls give finance teams the oversight they need without slowing down the employees doing the spending.

Most finance leaders have had the same experience: a company card program that was supposed to simplify things, but became its own administrative burden. Employees carry cards with shared limits, receipts go missing, and month-end reconciliation means hours of spreadsheet work trying to match charges to departments or projects.

The problem isn't that teams spend too much. The problem is that most card programs weren't built with finance teams in mind. Recent payment industry research found that the majority of cardholders, including business cardholders, feel indifferent or actively dissatisfied with their card experience. For personal spending, that might be a minor frustration, but for finance teams managing hundreds of transactions a month, it's a real operational problem.

Here's what's actually driving that dissatisfaction, and what a better card experience looks like for the teams managing business spend.

When CFOs and controllers describe their ideal card experience, the requests are remarkably consistent. They want to know who spent what before the month ends — not when the statement arrives. They want to issue spending authority quickly without handing out a shared corporate card. They want receipts collected automatically, not chased the week before close. And they want reconciliation to happen at transaction time, not billing time.

These aren't exotic requirements. They're the basics of financial control. But traditional card programs tend to deliver individual spending records without the workflow layer finance teams need. As we explored in one of our latest blog posts, real-time expense treal-time expense tracking: benefits beyond just visibility, the gap between when a transaction happens and when finance knows about it is where most expense management problems originate.

Traditional card programs have a few structural limitations that create ongoing friction for finance teams:

The result is a card program that generates data without generating control, which is precisely the opposite of what finance teams are trying to build.

Virtual cards are often described as "digital versions of physical cards", but that framing undersells what they do for finance teams. The meaningful difference isn't the format. It's the control layer.

With virtual cards through Extend, finance teams can issue a unique card to any employee or vendor in seconds, with per-card spend limits and expiration dates set before the card is ever used. When a charge posts, the receipt is already attached. When it's time to reconcile, the transaction flows automatically to your accounting system — whether that's QuickBooks, NetSuite, Xero, Sage Intacct, or Microsoft Dynamics.

This is what streamlining expense management actually looks like in practice: not just reporting on what happened, but controlling what can happen in the first place.

One of the most meaningful shifts virtual cards enable is connecting the full lifecycle of a business payment — from approval to reconciliation — without requiring finance to manually stitch together multiple systems.

With Extend, when an employee needs a card for a vendor or project, the request and approval happen in the app. The card is issued with the right limits already embedded. When the charge posts, the receipt is already attached. When it's time to close the books, transactions flow automatically to your accounting system.

The key shift is that work traditionally done at month-end — coding, categorizing, matching — gets distributed to the point of purchase, where context is still fresh and receipts are right at hand.

Extend also works on top of the business credit cards your company already has. That means you keep your existing bank relationship, your rewards programs, and your preferred credit lines. You're adding a control layer — not rebuilding your payment infrastructure.

Better card controls are only useful if they're enforced consistently. One reason expense policy compliance is hard to maintain is that policies live in a document, while spending happens in the real world — on travel booking sites, vendor portals, and online stores.

Virtual cards bridge that gap. When you issue a card with a specific limit, a specific vendor restriction, or a specific expiration date, the policy is embedded in the card itself. There's no room for an employee to accidentally overspend because the card simply won't authorize charges that exceed the parameters you've set.

This doesn't require employees to do anything differently — they use the card like any other credit card. The control happens at the infrastructure level, not through employee self-discipline. For teams building or updating their expense policies, expense policy best practices and templates for modern businesses walks through how to structure controls that work alongside virtual card programs like Extend.

For teams managing spend across multiple departments or locations, Extend also supports budget-level controls — grouping spend across multiple virtual cards under a single budget so you can see total burn against a project or cost center in real time.

The business card experience isn't just about the card itself — it's about the entire workflow surrounding how money moves through your organization. Most card programs deliver a payment mechanism. What finance teams need is a control layer.

Extend adds that control layer without requiring you to switch banks or rebuild your payment infrastructure. You keep your existing bank relationship, your credit lines, and your rewards programs. You add the per-card limits, real-time visibility, receipt capture, and accounting integrations your team actually needs to operate efficiently.

The result is a card program that works for finance — not one that creates extra work for it. Learn more about virtual employee cards with Extend and how spend controls give finance teams the oversight they need without slowing down the employees doing the spending.

Learn more about Extend and find out if it's the right solution for your business.

%201.png)

%201.png)